I think I left the teller at the bank genuinely disturbed when I told him that “If I can’t afford it, I just don’t buy it.” “What about a car? Do you drive a car?” he inquired, his voice toning on the edge of fear. I told him, “Yeah, I have a vehicle. I bought it used for under $3,000.” He looked physically pained. “What about if you want to buy some kind of new appliance? Or furniture?” he persisted. I stared at him blankly. “My couch was $5.00 at Goodwill. Like…I just buy shit cheap or I don’t buy it at all. The only thing in my life that I make payments on is my house, my bills, and my insurance, and that’s split five ways because I have housemates.” The young man looked horrified? Appalled? And somehow also awed? This guy couldn’t have been much older than me. But it seemed that he’d never even considered the option before of saving up for something to purchase it outright instead of using a credit card. Am I the only person in my general age group (just turned 26) who’s never owned a credit card, and who has forgone basic comforts in order to save up for items so you don’t owe money to anyone, like, ever?

If you’re living in the US without a credit card at 26, you’re playing with danger.

No credit is viewed as the same as bad credit. Which means you could be denied if you ever do need to rent an apartment or a car. Hospitals and clinics are also less likely to allow payment plan programs for people without good credit.

The best thing you could do at this point is apply for a credit card you’re eligible for and pay a few things (I do gas and groceries myself) with it each month. As long as you keep it to zero balance each month there is no interest and there will be proof of you not having debt (instead of just the absence of debt).

what.

This is legit how it works. The system requires records on you, or else. So you need a credit card and worse, you need to have a record of using it, even if you pay it off every single month. Unfortunately, the formulas used to determine credit score are secret, so we also have people suggesting that your credit rating is helped if every so often you do pay a bit of interest. The whole thing is a complete mess. If you don’t have a credit rating/history, then any loans you manage to get will be at extremely high interest and will require much more effort than they really should.

what

yeaah let me just go get a card that i can’t pay off because capitalism is shit, even if i literally only buy a pack of gum that’d go well

If you pay it off in full every month there is no interest. Do what OP is doing but put some of that on your credit card and pay it off every month, and soon you will have a very good credit rating.

you skipped right the fuck over the “can’t pay it off” part huh

like credit cards are just not a viable thing if you’re poor and have shit income

And I’m saying to literally not put anything on it if you can’t buy it in cash. And I’m aware that they fuck over poor people, but yeah, that’s the system that’s in place. This is advice for navigating it, which is how to obtain good credit which helps a lot.

Right like don’t make minimum payments, put your gas on your credit card then that same day pay the credit card company online then don’t worry about it for another month. It’s an absolutely shit system, but in the event of an emergency it’s good to have.

I have had to explain this to a lot of people in my life, but it’s true- no credit is the same as bad credit. What having (and using) the card actually shows is that you are capable of (and actually follow through on) making regular payments: ie, it is proof of having a steady income (even if you do not actually have a steady income). It is showing you reliably can pay for things you purchase, which is what your credit score is all about.

Think of it this way. You have a credit card, which is your credit tracking device. You use the card to tell someone “I will pay for this thing with borrowed money.” They agree to allow you to pay with borrowed money. You then turn around to your credit card company and say “Thank you for allowing me to borrow your money, I will now pay you back with my own money.” (which, if you repay them promptly enough, you can repay them the exact same amount you borrowed, rather than paying them more than you borrowed [which is what interest is])

The credit card company then recognizes that you successfully borrowed their money AND returned it safely, and they pass that information along to credit tracking companies. Each time you do this, you gain credibility. If you do this enough times, you are considered a credible borrower of money, so that if you ever are in a situation where you need to borrow a large sum of money (for example, a mortgage or a car or a hospital bill or whatever), companies with money will look at how well you have returned money in the past, and say Ah yes, this person repays their debts well, so we can lend them our money this time.

So like, do what the above folks are recommending. Get a credit card and use to to reasonably purchase things you already have to buy- put a batch of groceries on the card. Go home (or wherever you can use the interne), pay it off as if you had paid cash in the store for it. There is no extra fee or interest for doing this, and you are leveling up your credibility in case of emergency later on in life.

Ok, here’s a guide for the easiest way to do this.

1. get your first baby credit card with the bank that you already bank with. If it has cashback rewards, even better (that’ll be free money later).

2. set that shit up so it pays the full amount, automatically, every month. you don’t have to remember to go home and pay it off, or worry about it at all. You won’t pay interest.

Your first card, especially if you have no credit, is going to have a small limit. Like $500. This is important: credit companies want you to use a certain percentage of the card every month. This is 1-9%. I usually just go straight 5%. If you use too much, you look like a wild card (even if you pay it off every month) and if you use nothing than you’re not proving to them you can be trusted.

So your first card has a $500 limit. 5% of 500 is $25.

Your goal is to use $25/month.

This is about a tank of gas for me. So once a month, I would fill up with this card, and then put it in the back of my wallet until next month. The payment was made automatically by my bank from one account (debit) to the other (credit). Rinse and repeat. I did this for a year.

Then after a year, my credit had skyrocketed (because I had nothing before, and added this good habit for a year). So I called up my bank and asked for them to increase my limit based on my new credit. I had shown them I was good at borrowing a good amount of money and paying it back on time every time.

The bank increased my limit to $5,500. Like holy shit, at the time I was definitely not expecting that.

So new math. 5% of 5500 is $225. So now instead of gas, I put my cell phone bill ($50), my car insurance ($130), and my dog food automatic order ($40) on it.

The best part is everything is automatic. I keep this card in the back of my wallet permanently; all these bills and the automatic payments are, well, automatic. My credit goes up, I rack up cash back rewards, there’s nothing to it.

And, if I ever get in an emergency, like a vet bill for one of my dogs, I can use that card to pay the $3,000 emergency bill without worrying about whether the place will take my dog if I have no money. I can then go home, change the settings from “pay in full every month” to “pay $X every month” (more than the minimum!) until it’s paid off, and then go back to just my bills. My credit might take a little dip during that time, but will bounce back pretty quickly.

There’s several other factors to credit (hit me up if you want more info) but this was literally the only measure I took for my first year, and my credit went from 525 to 700 in a year. Another year later, I’m now at 753, have a mortgage with a great rate, and can get a monster ass loan if I really need it in case an emergency or hard times fall.

It’s a shitty system of hoops to jump through, but knowing you can use these measures if it comes to it is a good feeling.

KIDS. This is (unfortunately) BASIC ADULTING. Please go do the thing. There’s a ton of credit cards out there with 0 annual fees and even a loyalty program.

THEN live responsibly like OP

Also keep an ear out. Depending on where you bank, there may be short term incentive programs that offer pre-approvals for credit cards. I got my first card accepting an offer from my bank, a good rewards card with no annual fee, a 21 day grace period for interest, and a student interest rate. You may also get the same kind of offers to increase your credit limit without needing to make a formal appointment (though keep your eyes open, some credit card companies will automatically increase your limit)

And if you do online banking, check if your financial institution has an option to apply for a credit card online. It can save you an appointment if that gives you anxiety, and all the same information on interest rates and annual fees and rewards incentives, whether it be points or cash back, should be readily available on your bank’s website. Another option would be to call your bank’s advice line (there’s usually a 1-800 number on the back of your debit card, or find the number online) if you want to speak to someone but don’t want to or can’t make it into a branch.

And if you’re worried about ever finding yourself in a position where you will be unable to make payments, like loss of employment or serious injury, consider asking if your financial institution offers optional creditor insurance for your card (mine does, at a very reasonable premium) Some creditor insurance even offers rewards like free credit added to your card, or one time payments, for lifetime milestones like having a baby or getting married. So make sure you look into what all your options are.

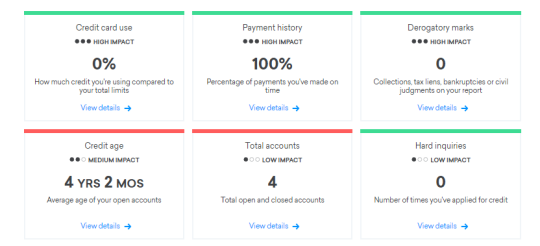

Also, if you’re not sure what your credit looks like, I can’t recommend Credit Karma enough. It really is free (I think they make money by offering people credit cards and so on) and allows you to check your credit score and see what accounts show up on it, etc. This is also a good way to make sure that you don’t have any fraudulent accounts on your credit report without having to pay a monthly fee for “fraud alerts” from the major credit reporting services. And, you can use their tools to see what you can do to improve your credit score, because it breaks your score down and gives you “grades” for the different areas (like number of accounts, age of accounts, etc) that go into your score. So you can see that, for instance, part of the reason your score is low is because you haven’t had your credit accounts very long, so you know that will go up just with time. Versus seeing that you have X-many credit accounts or whatever and that’s why it’s low, so you can think about opening a new one or closing one or more. It can also remind you of accounts you may have forgotten about, like that Target card you opened to get the 20% off discount seven years ago or whatever. Anyway, it’s really useful and it helped me raise my credit score by like 75 points, just by knowing what was going on and what I could do to improve it!

The idea of being in debt, even small amounts for brief periods, makes me physically nauseous. I’ve pretty much resigned myself to having a shit credit score forever, and simply failing at any interaction which requires a credit check. It’s entirely possible that I’ll die because somebody refuses to give me medical treatment without the approval of some meaningless number created by three big companies to measure how much money they expect to be able to siphon out of me. I accept this in the same way that I accept the inevitability of my identity being stolen because those three big companies have shit for network security and all the personal information they’re illegally gathering is stolen every few months.

Maybe someday we will move away from this increasingly idiotic system, but it won’t be for a long, long time.

More advice:

Do not close your oldest accounts or cards.

Even if you don’t use it and you’ve had it for years. Even if you’ve switched banks. A massive part of your credit score is rooted in the average age of your credits. Things like your student loans, car loans, credit cards, etc. Pay them off to just the brink (for loans) or keep their balance as low as possible (credit cards), but don’t end them until you have multiple accounts that are 7+ years old. This is easily the most important “bad thing” about my credit score.

Also, more accounts is obviously better, but it’s also dangerous to start too many accounts at the same time. Get a credit card when you turn 18 if you can handle it.

Get another credit card when you turn 21. Combined with your probably student loans (or car loan if you’re not going to college), this gives you three accounts that you can easily keep going for years and years if handled responsibly, and having them start at similar times means that losing or closing one of them (like a student loan) isn’t going to hurt your credit too much.

Yes, paying off your student loans entirely can hurt your credit. Because our system is dumb.

REITERATING that if you have an excellent credit score YOU CAN GET SHIT FOR CHEAPER, if you get a card with rewards, They PAY YOU a little bit to use the card at certain places, if you link it up with an airline miles app YOU CAN EARN MONEY FOR TRAVEL. Credit Cards are only an issue if you dont know how to safely use them without going overboard.

Seriously. As much as it is painful, buy a credit card and use it, even if you aren’t explicitly trying to raise your credit (though if you can, you should). They can be amazingly helpful to improving your livelihood as a whole, and if you treat it well and stay informed they can save your ass when you find yourself suddenly needing a lot of money really quickly.

I use my credit cared for bills at different times then pay almost everything on it off (because accruing tiny bits of interest helps your credit for dumb reasons) and it allows me to get things paid on my actual paycheck schedule rather than having every single bill due on the same day of the month. I hate that I have to give in to the system, but nothing make you fold like not having any money for real groceries because every penny you save is consumed by rent and other unexpected petty nonsense.

Adding my 2 cents: the strategy described works remarkably well. Even before I checked my credit score, I could tell I was doing well because, by way of immediately paying off small purchases monthly (and one time accruing interest on like $5), I’d managed to go from a basic, restrictive, $200 or something limit, to a much more adult-y and generous $2k one, in under half a year.

I’m not stupid, though; my monthly purchases with it have never gone past $100 ever and I don’t intend to change that.